RESEARCH AND DEVELOPMENT COSTS

SECTION 1: Definition of activities relating to research and development

An internally generated intangible asset may be capitalized if:

- It meets the definition of an asset and in particular that this fixed asset is identifiable

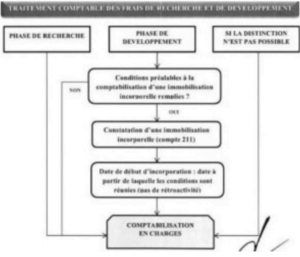

- We can distinguish the research phase from the development phase. Otherwise, all costs are expensed.

Research is defined as an original and planned investigation carried out by an entity with a view to acquiring new scientific or technical understanding and knowledge. We distinguish :

- Activities aimed at obtaining new knowledge

• The search for the application of research results or other knowledge as well as their evaluation and the choice ultimately made

• Research into other materials, devices, products, processes, systems or services

• The formulation, design, evaluation and final selection of alternative new or improved materials, devices, products, processes, systems or services.

Expenses incurred for research or during an internal research project must be recognized as an expense in the financial year during which they are incurred. However, if these expenses are incurred as part of a combination of entities, they are recognized as an intangible asset.

Development is the application of research results or other knowledge to a plan or model for the production of new or substantially improved materials, devices, products, processes, systems or services, before the commencement of their production. commercial production or use. We distinguish :

- Design, construction and pre-production or pre-use testing of models and prototypes

• Design of tools, templates, molds and dies involving new technology

• Design, construction and operation of a pilot unit which is not on a scale allowing commercial production under economic conditions

• Design, construction and testing for the chosen solution for other new or improved materials, devices, products, processes, systems or services.

SECTION 2: Accounting for development expenses

To recognize development expenditure as an intangible asset, the entity must complete

simultaneously the following conditions:

- The technical feasibility necessary for the completion of the intangible asset with a view to its commissioning or sale

• Its intention to complete the intangible asset and use or sell it

• Its ability to use or sell the intangible asset

• How the intangible asset will generate likely future economic benefits

• The availability of appropriate technical, financial and other resources to complete the development and use or sell the intangible asset

• Its ability to reliably assess the expenses attributable to the intangible asset during its development.

Otherwise, consider these expenses as charges.

This diagram below summarizes the operating procedure for accounting development costs.

Development costs are recognized by debiting account 211_development costs and crediting account 721_capitalized production, intangible assets.

Subsequent expenses incurred and relating to a research and development project must be accounted for according to the same principles as those relating to internally generated research and development projects.

Concerning the amortization of capitalized development costs, it must be spread over the life of the asset in question. It is recorded in the debit of account 6812_Allocations to depreciation of intangible assets, and by the credit of account 2811_Amortization of development costs.

SECTION 3: Evaluation of development expenditure

The development cost is measured from the date on which this intangible asset first meets the recognition criteria. However, expenses recognized as an expense prior to the activation date can no longer be activated.

Development costs include all expenses directly attributable to the development of this intangible asset. These are the costs necessary for the creation, production and preparation of the fixed asset. We distinguish :

- The costs of materials and services used or consumed to generate the intangible asset

• The costs of employee benefits resulting from the creation of the intangible asset

• Fees for registering a legal right, such as a patent

• Functional testing of the asset

• Amortization of patents and licenses used to generate the intangible asset

• Borrowing costs as long as they meet the criteria for capitalizing borrowing costs, to be included in the costs of an internally generated intangible asset.

However, launch costs (advertising), administrative and overhead costs, clearly identified inefficiencies, and initial operational losses, expenses for training staff to use the asset are to be excluded from directly attributable costs.

SECTION 4: Research and development expenses carried out within the framework of orders from third parties

R&D costs concern expenses made by the entity in this area for its own account. Therefore, any other costs included in the production cost of orders placed by third parties must be included as expenses.

SECTION 5: Derecognition or exit of development costs

An intangible asset must be derecognized upon disposal or when the entity no longer expects future economic benefits from its use or disposal.

In the event of failure of the R&D project or when the conditions for activating expenses are not met, previously capitalized development costs are immediately removed from the asset. In fact, we debit account 2811_Amortization of development costs and account 81_Carrying value of fixed asset transfers for the fraction of development costs not yet amortized. And we credit account 211_Development costs.

Also when R&D costs are used to create a tangible asset (prototype), they are recorded in the fixed asset or inventory account and not in account 211 development costs.

SECTION 6: INFORMATION TO BE PROVIDED

At the balance sheet level, the normal system includes an intangible asset item to indicate the amount of R&D costs.

It is also appropriate to provide the necessary information in the accompanying notes if it is significant.

The management reports provided by capital companies necessarily provide R&D activities and forecasts.

PATENTS, LICENSES, TRADEMARKS, SOFTWARE, WEBSITES AND OTHER SIMILAR RIGHTS

SECTION 1: PATENTS, LICENSES AND SIMILAR RIGHTS

- A patent is a title giving the inventor of a product or process capable of industrial applications, or its assignee, a monopoly of exploitation for a certain time. A patent can either be acquired or generated internally. When acquired, it is recorded at acquisition cost and debited to account 221_Patents.

In the case where it is generated internally, patent creation costs are capitalized when they meet the conditions to be recognized as development costs.

When the granting of a patent follows research linked to the realization of projects, account 2121_Patents is debited with the amount corresponding to the costs incurred during the development period including patent filing fees, by crediting account 211_Expenses of development.

Patents are amortizable over the duration of protection they benefit from or over their effective duration of use.

- The operating license is an act by which the owner of a brand gives a third party the possibility of selling one or more of its products for a fee. They are to be recorded as fixed assets at the acquisition cost and debited to account 2122_Licences.

However, when it is acquired by means of annual royalties composed of a fixed part and a variable part, the recognition of the fixed part is recorded on the assets side of the balance sheet in return for the recording of the debt on the liabilities side. . And the variable part will be recognized as an expense over each of the financial years.

The amortization of the license must be calculated over the probable duration of use which cannot exceed the duration of the authorization at the end of which the residual value will be zero.

- Public exclusive rights are exclusive rights for payment or free of charge granted by an administrative authority (licenses, import quotas, landing rights at an airport, etc.). Exclusive rights for payment are recorded at their acquisition cost if they are acquired for a period of more than 12 months. On the other hand, those acquired free of charge are recorded at their current value (which is rarely possible). Therefore, as a precautionary principle, SYSCOHADA considers them to have zero value. Depreciation must be calculated over the useful life which must not exceed the contractual duration.

SECTION 2: SOFTWARE

Software constitutes legally protected intangible rights. It is important to distinguish:

- Software inseparable from hardware:Like operating systems and other integrated software, they are recognized as tangible assets with the hardware to which they are attached.

- Software that is part of a development project:This software therefore follows the accounting treatment of the projects to which they relate. Costs incurred during the research phase are recognized as an expense and those incurred during the development phase are capitalized.

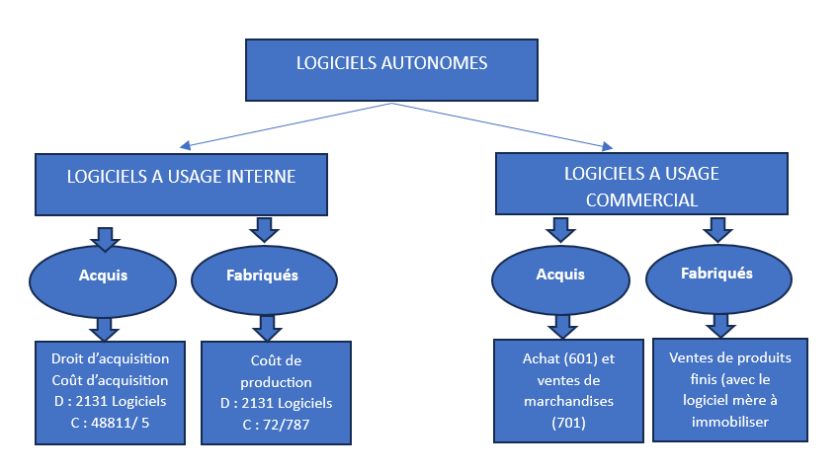

- Standalone softwares: For this case, we distinguish:

Expenditures made to improve software can either be capitalized or recognized as expenses.

SECTION 3: Websites

Depending on the acquisition process, there are

- Websites acquired “turnkey”: which must be recognized as fixed assets at their acquisition cost by debiting account 2132_Internet sites. However, if the acquisition cost is very low, they can be charged. It must be depreciated on a straight-line basis over its probable useful life.

- Websites created by the entity: these are advertising sites and e-commerce sites and similar:

Site (s | Definition | Accounting |

“Advertising” sites | Sites constituting simple presentations of information relating to identity. | Expenses are left in charges |

“E-commerce” sites | Sites recording customer orders and/or participating in the entity's information or commercial systems. | The expenses are immobilized if the conditions for activating development costs are met |

The design and development of e-commerce sites involves 3 phases:

- Preliminary research phase: the costs incurred during this phase must be borne, because there is not yet visibility on the future economic benefits.

- Development and production phase: the costs incurred throughout this phase are recorded as assets in the debit of account 2132_Internet sites.

- Operation phase: Expenditures subsequently incurred after the acquisition or completion of the site are to be recognized as expenses, unless there is a probability that these expenses will enable the site to generate future economic benefits and also that these expenses can be evaluated and attributed to the asset in a reliable manner.

SECTION 4: Trademarks

We distinguish :

- The brands acquired: are recognized as fixed assets and depreciable if the useful life is determinable. Consequently, brands with legal protection are generally non-depreciable.

- Brands created in-house: the expenses incurred for the creation of this brand are recognized as an expense.

SECTION 5: Right to lease and doorstep

The lease right constitutes an intangible asset for the tenant who pays it, which must be amortized over the term of the lease.

The door pass is an additional rent spread over the duration of the lease and therefore constitutes an expense to be recorded in the Rental account. At the end of the financial year, the rent supplement relating to the following financial years is reversed by the CCA account.

SECTION 6: Customer files notices newspaper titles and magazines

- When acquired, they are recorded as fixed assets and amortized over the useful life of the file, notices, newspapers or magazines. However, if the customers on the list are supposed to remain with the entity (leadership position, niche, etc.), no amortization.

- When generated internally; they are recognized as an expense, due to the impossibility of distinguishing them from those incurred to develop the activity of the entity as a whole.

SECTION 7: Commercial funds

It is a set of means (tangible and intangible), allowing a merchant to attract and retain customers. The elements of the goodwill are accounted for according to their nature and the residual element not allocated to a specific account is recorded as a debit to the goodwill account. If it is created by the entity, it is registered in charge.

It is in principle non-depreciable, because it has an unlimited lifespan. If its useful life is limited, it is depreciable. In exceptional cases where the duration is limited, but cannot be reliably estimated, it is amortized over 10 years.

However, it must undergo impairment tests whenever an indication of loss of value appears.

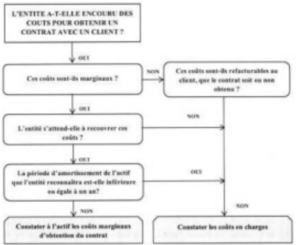

SECTION 8: Cost of obtaining the contract

These costs are activated if the following conditions are met: