FRAIS DE RECHERCHE ET DEVELOPPEMENT

SECTION 1 : Définition des activités relatives à la recherche et au développement

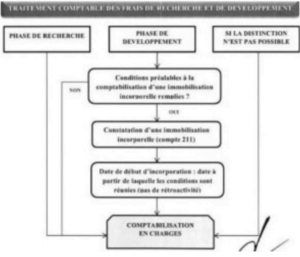

Une immobilisation incorporelle générée en interne est susceptible d’être inscrite à l’actif si :

- Elle répond à la définition d’un actif et notamment que cette immobilisation est identifiable

- On arrive à distinguer la phase de recherche de la phase de développement. Sinon, l’intégralité des coûts est en mettre en charges.

La recherche est définie comme une investigation originale et programmée réalisée par une entité en vue d’acquérir une compréhension et des connaissances scientifiques ou techniques nouvelles. On distingue :

- Les activités visant à obtenir de nouvelles connaissances

• La recherche de l’application de résultats de recherche ou d’autres connaissances ainsi que leur évaluation et le choix retenu in fine

• La recherche d’autres matériaux, dispositifs, produits procédés, systèmes ou services

• La formulation, la conception, l’évaluation et le choix final d’autres possibilités de matériaux, dispositifs, produits, procédés, systèmes ou services nouveaux ou améliorés.

Les dépenses supportées pour la recherche ou lors d’un projet de recherche en interne doivent être comptabilisées en charge de l’exercice au cours duquel, elles sont encourues. Toutefois, si ces dépenses sont encourues dans le cadre d’un regroupement d’entités, elles sont comptabilisées en immobilisation incorporelle.

Le développement est l’application des résultats de la recherche ou d’autres connaissances à un plan ou un modèle en vue de la production de matériaux, dispositifs, produits, procédés, systèmes ou de services nouveaux ou substantiellement améliorés, avant le commencement de leur production commerciale ou de leur utilisation. On distingue :

- Conception, construction et tests de pré-production ou de pré-utilisation de modèles et prototypes

• Conception d’outils, de gabarits, moules et matrices impliquant une technologie nouvelle

• Conception, construction et exploitation d’une unité pilote qui n’est pas à une échelle permettant une production commerciale dans les conditions économiques

• Conception, construction et tests pour la solution choisie pour d’autres matériaux, dispositifs, produits, procédés, systèmes ou services nouveaux ou améliorés.

SECTION 2 : Comptabilisation des dépenses de développement

Pour comptabiliser les dépenses de développement en tant qu’immobilisation incorporelle, l’entité doit remplir

simultanément les conditions suivantes :

- La faisabilité technique nécessaire à l’achèvement de l’immobilisation incorporelle en vue de sa mise en service ou de sa vente

• Son intention d’achever l’immobilisation incorporelle et de l’utiliser ou de la vendre

• Sa capacité à utiliser ou à vendre l’immobilisation incorporelle

• La façon dont l’immobilisation incorporelle générera des avantages économiques futurs probables

• La disponibilité de ressources techniques, financières et autres, appropriées pour achever le développement et utiliser ou vendre l’immobilisation incorporelle

• Sa capacité à évaluer de manière fiable les dépenses attribuables à l’immobilisation incorporelle au cours de son développement.

A défaut, considérer ces dépenses comme des charges.

Ce schéma ci-dessous résume le mode opératoire de traitement comptables des frais de développement.

Les frais de développement sont comptabilisés en débitant le compte 211_frais de développement et en créditant le compte 721_production immobilisée, immobilisations incorporelles.

Les dépenses ultérieures engagées et qui concerne un projet de recherche et de développement, doivent être comptabilisées selon les même principes que celle relative aux projets de recherche et développement générés en interne.

Concernant l’amortissement des frais de développement immobilisés, il doit être étalé sur la durée de vie de l’actif considéré. Il est comptabilisé au débit du compte 6812_Dotations aux amortissements des immobilisations incorporelles, et par le crédit du compte 2811_Amortissement des frais de développement.

SECTION 3 : Evaluation des dépenses de recherche et développement

Le coût de développement se mesure à partir de la date à laquelle, cette immobilisation incorporelle satisfait pour la première fois aux critères de comptabilisation. Toutefois, les dépenses comptabilisées en charge antérieurement à la data d’activation ne peuvent plus être activées.

Les coûts de développement englobent toutes les dépenses directement attribuables au développement de cette immobilisation incorporelle. Ce sont les couts nécessaires à la création, la production et la préparation de l’immobilisation. On distingue :

- Les coûts de matériaux et services utilisés ou consommés pour générer l’immobilisation incorporelle

• Les coûts des avantages du personnel résultant de la création de l’immobilisation incorporelle

• Les honoraires d’enregistrement d’un droit légal, tel qu’un brevet

• Les tests de fonctionnement de l’actif

• L’amortissement des brevets et licences utilisés pour générer l’immobilisation incorporelle

• Les coûts des emprunts dès lors qu’ils satisfont aux critères d’activation des coûts d’emprunt, pour être inclus dans les coûts d’une immobilisation incorporelle générée en interne.

Cependant, les coûts de lancement (publicités), les coûts administratifs et frais généraux, les inefficacités clairement identifiées, et pertes opérationnelles initiales, les dépenses au titre de formation du personnel pour utiliser l’actif sont à exclure des coûts directement attribuables.

SECTION 4 : Dépenses de recherche et développement réalisées dans le cadre de commandes des tiers

Les frais R&D concernent les dépenses réalisées par l’entité, dans ce domaine pour son propre compte. Donc, tout autre frais entrant dans le cout de production des commandes passées par des tiers sont à inscrire en charge.

SECTION 5 : Décomptabilisation ou sortie des frais de développement

Une immobilisation incorporelle doit être décomptabilisé lors de sa sortie ou lorsque l’entité n’attend plus d’avantages économiques futurs de son utilisation ou de sa sortie.

En cas d’échec du projet de R&D ou lorsque les conditions d’activation des dépenses ne sont pas réunies, les frais de développement antérieurement immobilisés sont immédiatement sortis de l’actif. En effet, on débite le compte 2811_Amortissement des frais de développement et le compte 81_Valeur comptable des cessions d’immobilisation pour la fraction des frais de développement non encore amortie. Et on crédite le compte 211_Frais de développement.

Aussi lorsque les frais de R&D servent à créer un bien corporel (prototype), ils sont enregistrés au compte d’immobilisation ou de stock et non au compte 211 frais de développement.

SECTION 6 : INFORMATION A FOURNIR

Au niveau du bilan, le système normal comporte un poste d’immobilisation incorporelle pour indiquer le montant des frais de R&D.

Il convient aussi de fournir dans les notes annexes les informations nécessaires si elles sont significatives.

Les rapports de gestion fournis par les sociétés de capitaux fournissent obligatoirement les activités et les prévisions en matière de R&D.

BREVETS, LICENCES, MARQUES, LOGICIELS, SITES INTERNET ET AUTRES DROITS SIMILAIRES

SECTION 1 : BREVETS, LICENCES ET DROITS SIMILAIRES

- Le brevet est un titre donnant à l’inventeur d’un produit ou d’un procédé susceptible d’applications industrielles, ou à son cessionnaire, un monopole d’exploitation pendant un certain temps. Un brevet peut être soit acquis, soit générés en interne. Lorsqu’il est acquis, il est comptabilisé au coût d’acquisition au débit du compte 221_Brevets.

Dans le cas où il est généré en interne, les frais de création de brevets sont immobilisés lorsqu’ils remplissent les conditions pour être comptabilisés en frais de développement.

Lorsque la prise de brevet est consécutive à des recherches liées à la réalisation de projets, le compte 2121_Brevets est débité du montant correspondant aux coûts engagés au cours de la période de développement y compris les frais de dépôt du brevet, par le crédit du compte 211_Frais de développement.

Les brevets sont amortissables sur la durée de protection dont ils bénéficient ou sur leur durée effective d’utilisation.

- La licence d’exploitation est un acte par lequel le propriétaire d’une marque donne à un tiers la possibilité de vendre un ou plusieurs de ses produits moyennant une redevance. Elles sont à comptabiliser en immobilisation au cout d’acquisition au débit du compte 2122_Licences.

Cependant lorsqu’elle est acquise au moyen de redevances annuelles composées d’un partie fixe et d’une partie variable, la comptabilisation de la partie fixe s’inscrit à l’actif du bilan en contrepartie de l’inscription de la dette au passif. Et la partie variable sera comptabilisé en charge sur chacun des exercices.

L’amortissement de la licence doit être calculé sur la durée probable d’utilisation qui ne peut excéder la durée de l’autorisation à l’issue de laquelle la value résiduelle sera nulle.

- Les droits d’exclusivité publics sont des droits exclusifs à titre onéreux ou à titre gratuit accordés par une autorité administrative (licences, quotas d’importation, droits d’atterrissage sur un aéroport…). Les droits d’exclusivité à titre onéreux sont comptabilisés à leur coût d’acquisition s’ils sont acquis pour une durée supérieure à 12 mois. En revanche, ceux acquis à titre gratuit sont comptabilisés à leur valeur actuelle (ce qui est rarement possible). Donc par principe de prudence, le SYSCOHADA les considère comme ayant une valeur nulle. L’amortissement doit être calculé sur la durée d’utilité qui ne doit pas excéder la durée contractuelle.

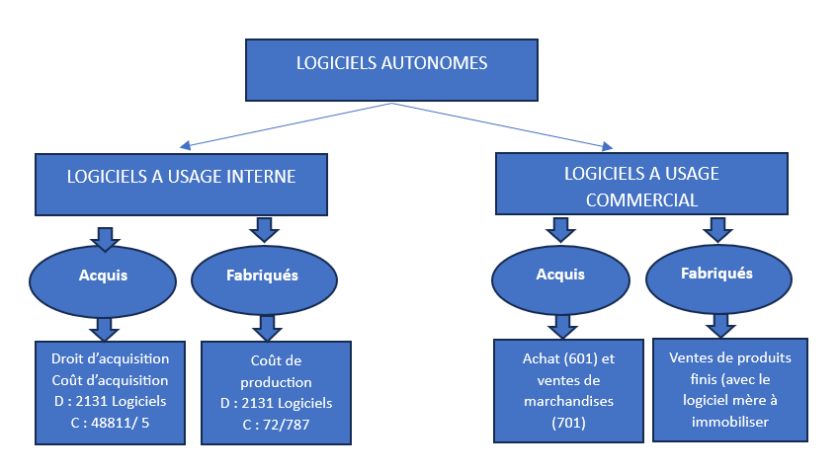

SECTION 2 : LOGICIELS

Les logiciels constituent des droits incorporels protégés juridiquement. Il convient de distinguer :

- Les logiciels indissociables du matériel : à l’exemple des systèmes d’exploitation et autres logiciels intégrés, ils sont comptabilisés en immobilisation corporelle avec le matériel auquel ils sont rattachés.

- Les logiciels faisant parti d’un projet de développement : Ces logiciels suivent dès lors le traitement comptable des projets auxquels ils se rapportent. Les coûts engagés durant la phase de recherche sont comptabilisés en charge et les ceux engagés durant la phase de développement sont activés.

- Les logiciels autonomes : Pour ce cas, on distingue :

Les dépenses faites en vues d’améliorer des logiciels peuvent être soit immobilisées, soit comptabilisées en charges.

SECTION 3 : Sites internet

Selon le processus d’acquisition, il existe

- Les sites internet acquis « clé en mains » : qui doit être comptabilisés en immobilisation à leur coût d’acquisition par le débit du compte 2132_Sites internet. Toutefois, si le fout d’acquisition est très faible, ils peuvent être portés en charge. Il doit être amorti selon le mode linéaire sur sa durée probable d’utilisation.

- Les sites internet crée par l’entité : il s’agit des sites publicitaires et des sites de e-commerce et assimilés :

|

Sites |

Définition |

Comptabilisation |

|

Sites « publicitaires » |

Sites constituant de simples présentations d’informations relatives à l’identité. |

Les dépenses sont laissées en charges |

|

Sites « e-commerce » |

Sites enregistrant des commandes clients et/ou participant aux systèmes d’information ou commerciaux de l’entité. |

Les dépenses sont immobilisées si les conditions d’activation des frais de développement sont réunies |

La conception et le développement de sites e-commerce comportent 3 phases :

- Phase de recherche préalable : les coûts engagés lors de cette phase sont à mettre en charge, car il n’y a pas encore une visibilité sur les avantages économiques futurs.

- Phase de développement et de mise en production : les coûts engagés tout au long de cette phase sont inscrits à l’actif au débit du compte 2132_Sites internet.

- Phase d’exploitation : Les dépenses ultérieurement réalisées après l’acquisition ou l’achèvement du site sont à comptabiliser en charges, sauf s’il y’a probabilité que ces dépenses permettent au site de générer des avantages économiques futures et aussi que ces dépenses puissent être évaluées et attribuées à l’actif de façon fiable.

SECTION 4 : Marques

On distingue :

- Les marques acquises : sont comptabilisées en immobilisation et amortissable si la durée d’utilité est déterminable. En conséquence les marques ayant une protection juridique sont en général non amortissable.

- Les marques créées en interne : les dépenses engagées pour la création de cette marque sont comptabilisées en charge.

SECTION 5 : Droit au bail et pas-de-porte

Le droit au bail constitue pour le locataire qui le verse une immobilisation incorporelle, qui doit être amorti sur la durée du bail.

Le pas-de-porte est un supplément de loyer réparti sur la durée du bail et constitue donc une charge à comptabiliser dans le compte Location. En fin d’exercice, le supplément de loyer concernant les exercices suivants est extourné par le compte CCA.

SECTION 6 : Fichiers clients notices titres de journaux, et magazines

- Lorsqu’ils sont acquis, ils sont comptabilisés en immobilisation, et amorti sur la durée d’utilité du fichier, notices, journaux ou magazines. Toutefois, si les clients de la liste sont censés rester acquis à l’entité (position de leader, niche…), pas d’amortissement.

- Lorsqu’ils sont générés en interne ; ils sont comptabilisés en charge, dus à impossibilité de distinction de celles engagées pour développer l’activité de l’entité dans son ensemble.

SECTION 7 : Fonds commercial

C’est un ensemble de moyens (corporels et incorporels), permettant à un commerçant d’attirer et de conserver une clientèle. Les éléments du fond de commerce sont comptabilisés selon leur nature et l’élément résiduel non affecté à un compte spécifique est inscrit au débit du compte fond commercial. S’il est créé par l’entité, il est inscrit en charge.

Il est en principe non amortissable, parce qu’ayant une durée de vie illimitée. Si sa durée d’utilité est limitée, il est amortissable. Dans les cas exceptionnels où la durée est limitée, mais ne peut être estimée de manière fiable, on l’amortit sur 10ans.

Il doit cependant subir des tests de dépréciation à chaque qu’apparait un indice de perte de valeur.

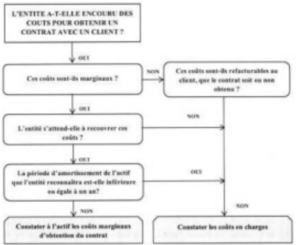

SECTION 8 : Coût d’obtention du contrat

Ces coûts sont activés si les conditions suivantes sont réunies :

Besoin d’aide dans la gestion de votre comptabilité ? Contactez notre équipe Expertise Comptable & Tax .